The downturn in the UK manufacturing sector showed signs of easing during August, following a severe contraction in the previous month. The seasonally adjusted Markit/CIPS Purchasing Manager's Index (PMI) rose to 49.5, from 45.2 in July, a four-month high and only slightly below the 50.0 mark that separates expansion from contraction.

The downturn in the UK manufacturing sector showed signs of easing during August, following a severe contraction in the previous month. The seasonally adjusted Markit/CIPS Purchasing Manager's Index (PMI) rose to 49.5, from 45.2 in July, a four-month high and only slightly below the 50.0 mark that separates expansion from contraction.

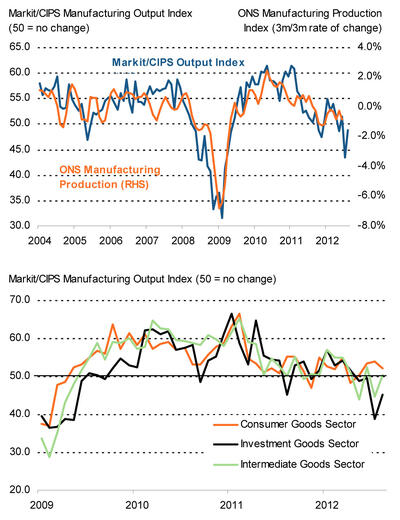

Manufacturing production fell for the second successive month in August, albeit to a much lesser degree than in July. The decline in output was centred on the investment goods sector. Output rose solidly at consumer goods producers, while intermediate goods companies saw a marginal return to growth.

The main factor underlying the downturn in production during recent months has been weak market conditions. Although August saw inflows of new work hold broadly steady at July levels, this followed four consecutive months of contraction. The broad stagnation of new orders was still a marked improvement on the severe decline seen in the prior month as companies reported a modest increase in new work from domestic clients. The rate of decline in new export orders also eased sharply, despite weak demand from Europe.

Manufacturing employment rose slightly for the second successive month in August. Payroll numbers were increased at SMEs, but continued to fall at large-scale producers. Where an increase in employment was reported, this mainly reflected ongoing efforts to clear backlogs of work. Average input costs declined for the third month running during August, reflecting lower metal and plastic prices. There were also reports that weaker demand for raw materials and exchange rate factors had reduced the cost of certain inputs. However, the rate of deflation eased sharply, mainly due to higher prices for oil and related by-products.

Manufacturing employment rose slightly for the second successive month in August. Payroll numbers were increased at SMEs, but continued to fall at large-scale producers. Where an increase in employment was reported, this mainly reflected ongoing efforts to clear backlogs of work. Average input costs declined for the third month running during August, reflecting lower metal and plastic prices. There were also reports that weaker demand for raw materials and exchange rate factors had reduced the cost of certain inputs. However, the rate of deflation eased sharply, mainly due to higher prices for oil and related by-products.

UK manufacturers continued to raise their average selling prices in August, reflecting efforts to recover some of the margin lost earlier in the year. Output charges have now increased throughout the past 34 months. However, the rate of inflation was only modest as strong competition and weak demand restricted the pricing power of a number of firms.

UK manufacturers continued to raise their average selling prices in August, reflecting efforts to recover some of the margin lost earlier in the year. Output charges have now increased throughout the past 34 months. However, the rate of inflation was only modest as strong competition and weak demand restricted the pricing power of a number of firms.

August saw manufacturers maintain a preference for reduced holdings of both pre- and post-production inventories. Purchasing activity was also scaled-back. Lower demand for raw materials reduced the pressure on supplier capacity, leading to a further shortening of vendor delivery times. Improved lead times also reflected successful negotiations with suppliers.

Rob Dobson, Senior Economist at Markit and author of the Markit/CIPS Manufacturing PMI, said: "The marked easing in the rate of contraction at UK manufacturers is heartening, if only because last month's steep pace of decline wasn't repeated. A further slight increase in employment was also a positive, while the domestic market held its ground, particularly in the consumer goods sector.

"However, having followed such marked declines in July, the August readings for production and new orders do little to change the underlying picture of a fragile sector facing enormous headwinds. Overall demand remains too lacklustre to provide an imminent and sustained recovery, with investment spending still weak and domestic austerity ongoing. Long unsatisfied hopes that the manufacturing sector could export its way back to health also remained jilted by the marrying of a downturn in our largest export market to the onset of softer global economic growth. The performance of the sector is therefore likely to remain subdued and volatile until underlying structural imbalances are resolved."

David Noble, Chief Executive Officer at the Chartered Institute of Purchasing & Supply, added: "We can take consolation from August's figures in that they were 'less bad' than the disastrous month before. We have witnessed a return to the status quo of flat growth in a fragile economy. This is a positive in itself, as a repeat of last month's performance would have been unthinkable. Also encouraging is the output growth in the consumer and intermediate goods sector, more so when taken alongside a marked easing in the rate of contraction at investment goods producers.

"This optimism however, is set firmly in the context of a slowing global economy. The UK manufacturing sector continues to struggle against economic headwinds, especially from Europe. Inevitably this picture continues to influence new export orders negatively, though the rate of this contraction eased significantly. At the same time, domestic new orders have rallied offering respite to the sector, which looks set for a long, flat recovery."

Add a Comment

No messages on this article yet